Highlight

Successful together – our valantic Team.

Meet the people who bring passion and accountability to driving success at valantic.

Get to know usApril 2, 2025

The EU Commission has presented a proposal to simplify important sustainability regulations. This article highlights the changes to the CSRD (Corporate Sustainability Reporting Directive) and explains why sustainability continues to play a key role for companies.

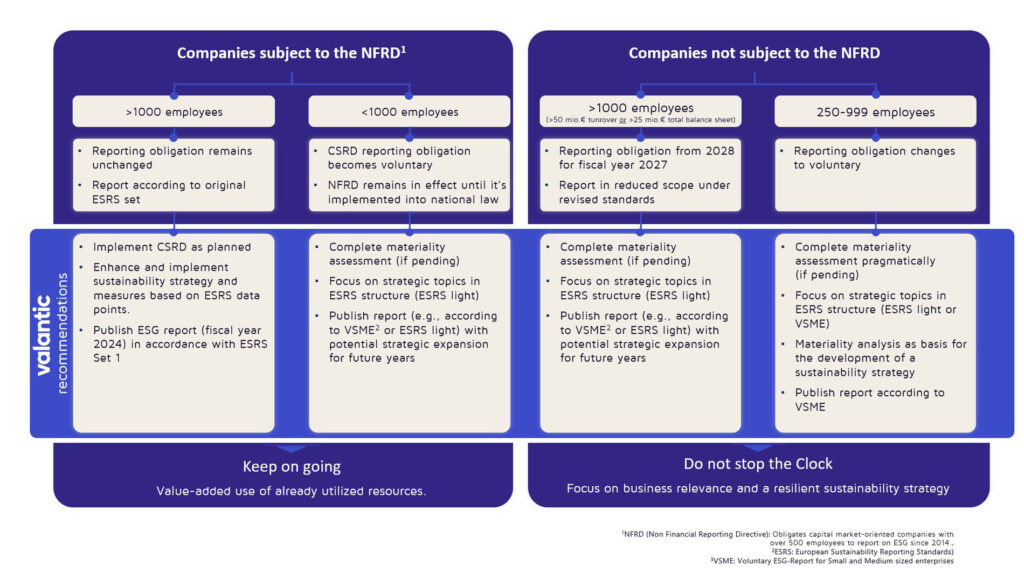

The Omnibus Regulation contains simplifications of the CSRD (Corporate Sustainability Reporting Directive), the CSDDD (Corporate Sustainability Due Diligence Directive), the EU Taxonomy and the CBAM Regulation (Carbon Border Adjustment Mechanism). But what does this mean for companies in concrete terms? Does the simplification of reporting reduce the relevance of sustainability or does it rather offer new opportunities?

Does the simplification of regulation and reporting requirements mean that sustainability is becoming less relevant for companies? On the contrary! Sustainability remains a key success factor. After all, customers, investors and banks are demanding ESG criteria and sustainability data, regardless of whether there is a legal obligation or not. Also, climate change – caused by extreme weather events or resource scarcity, for example – represents a potential business risk regardless of strict regulation.

Shaping the future with responsibility

valantic’s ESG consulting accompanies companies towards sustainable performance and strengthens social and ecological competence.

The new EU regulation proposal should therefore not be taken as a reason to stop sustainability activities. Since the EU Omnibus Regulation has not yet been transposed into EU law, changes are still possible and the existing law continues to apply. There is also now an opportunity to make focused use of resources already invested and knowledge already gained. Companies should identify, analyze and strategically use relevant data points in order to develop a future-oriented and sustainable corporate strategy.

Our recommendation is thus not to abandon all activities at this stage, but to switch focus – moving from purely compliance towards a focused, strategic sustainability orientation.

We’re here to help you find the best options and support you throughout – feel free to contact us!

The information provided on this website does not constitute legal advice and is not intended to address any legal issues or problems that may arise in individual cases. The information on this website is of a general nature and is provided for informational purposes only. If you need legal advice for your individual situation, you should seek the advice of a qualified attorney.

Marco Fuhr

Managing Consultant

valantic Supply Chain Excellence

Don't miss a thing.

Subscribe to our latest blog articles.